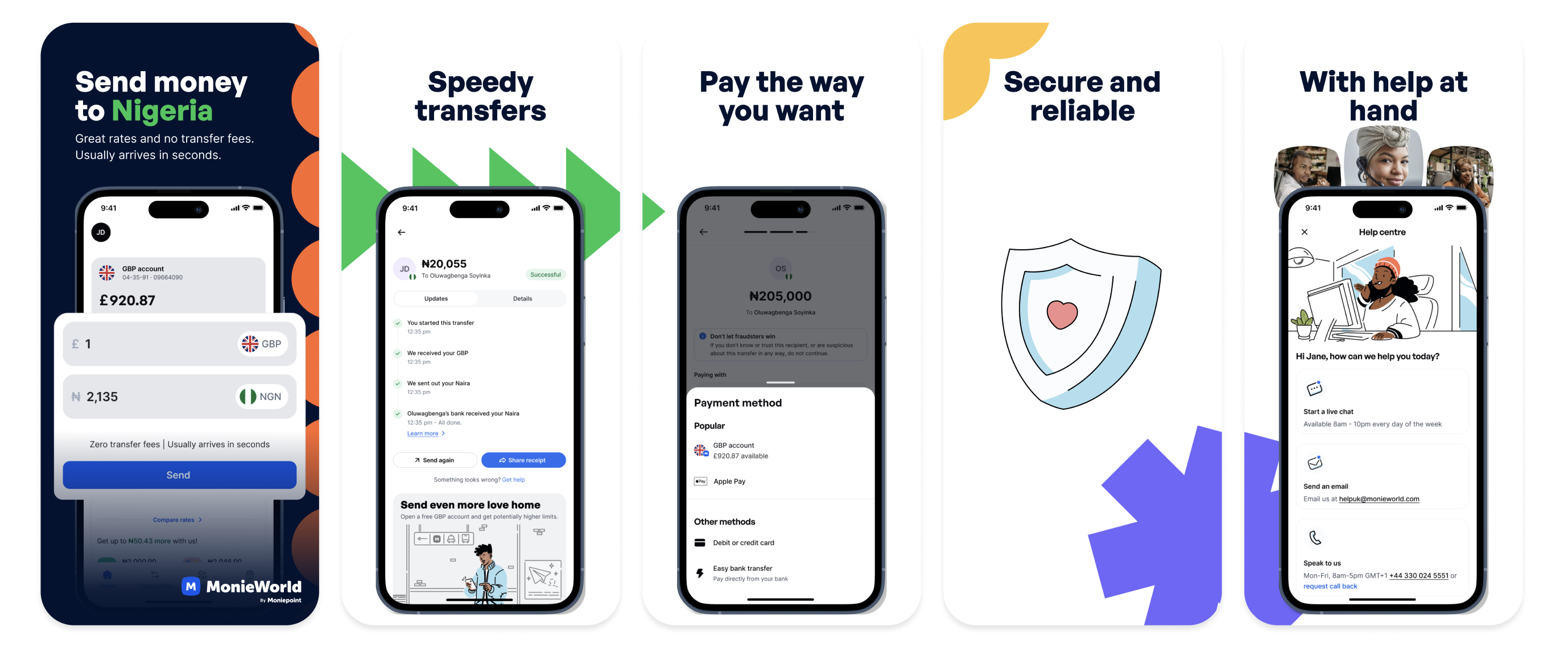

Designed the UK-to-Nigeria money corridor that beat the market from day one.

MonieWorld is Moniepoint's first international product — a GBP-to-NGN remittance app entering a market where LemFi holds 80–90% share. As Head of Product Design, I shaped the complete user experience across onboarding, home, and information architecture, while navigating an entirely new cultural and economic context for the first time.

RoleHead of Product Design

PlatformiOS · Android · Web

ShippedApril 2025

84.5%Signup conversion rate vs 20–25% industry average

20KUnique signups 3 months since launch (Apr–Jun 2025)

£7.6MTPV in the first 30 days UK-to-Nigeria FX corridor

Context

A new market, a new culture, and a team to build from day one.

MonieWorld is built for the Nigerian diaspora in the UK — a community that sends billions home each year and knows exactly which apps are fast, which are cheap, and which waste their time. LemFi dominates this corridor with 80–90% market share. Entering it meant the product had to earn trust immediately.

I joined as Head of Product Design three months before launch. My mandate was to ensure every design shipped met the standard — and to define what that standard looked like. Alongside delivery, I was responsible for hiring the remaining design team (a second designer, a content designer, and a researcher), shaping the product roadmap, and establishing the PED processes the team would work within.

There was also a dimension to this role I hadn't encountered before. My experience had been built across Asia and Europe — digitally sophisticated markets, high financial literacy, users shaped by Revolut, Apple Pay, and Wise. MonieWorld's users brought a completely different relationship with money and mobile: trust earned differently, priorities ordered differently, and a set of cultural signals I had to understand before I could design for. Learning that context — quickly and with humility — was its own work in the first weeks on the job.

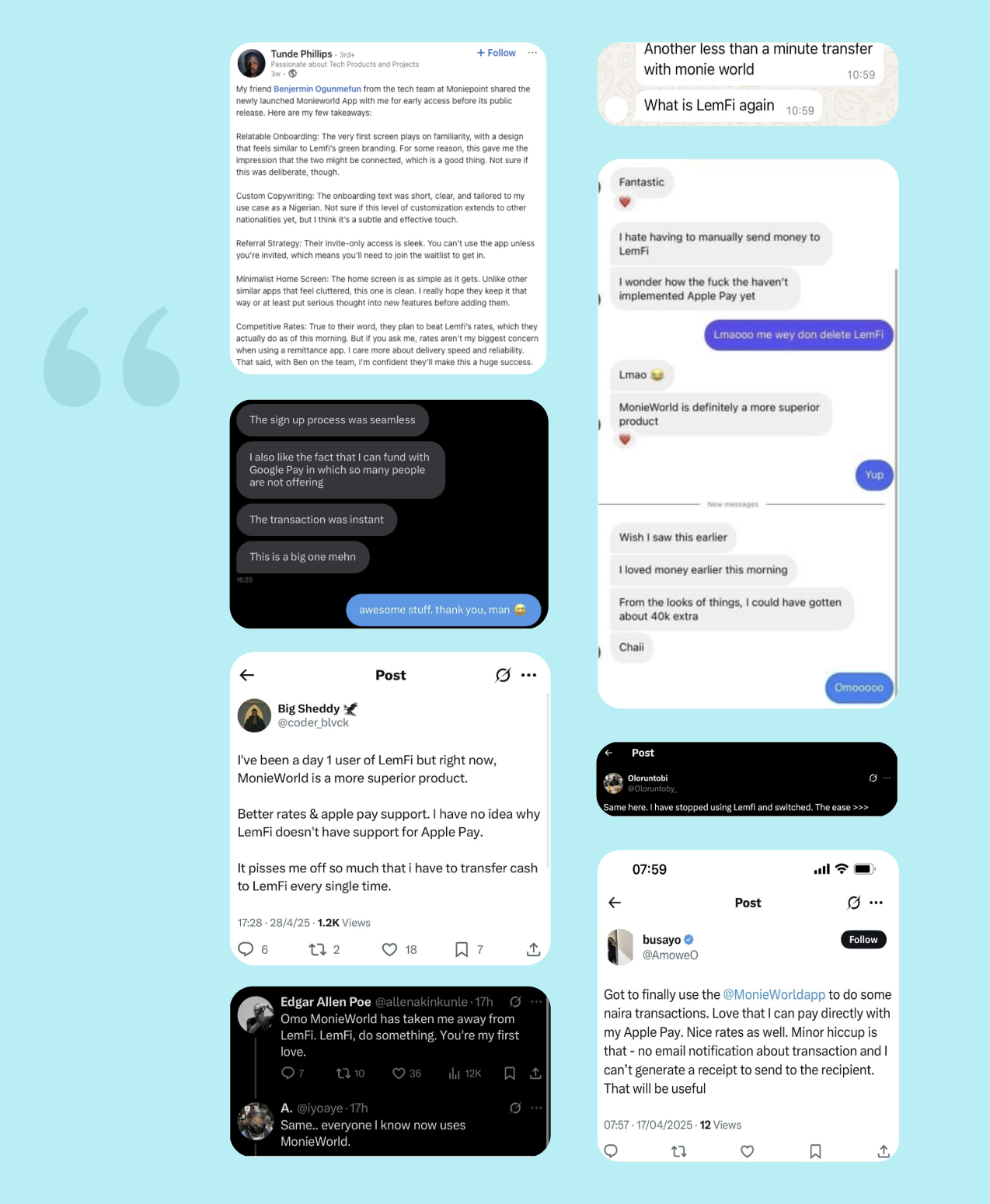

Overwhelmingly positive user feedback captured post-launch — the diaspora community responding to the seamless onboarding, and a complete remittance experience upgrade compared to LemFi.

#1 · Seamless Signup

We had feature parity with LemFi. We didn't have UX parity with Revolut.

Before I joined, the product had been designed largely in LemFi's shadow. Feature parity was a sound strategic decision — if you're entering a market where one app holds 80–90% share, you need to match its core functionality on day one. But functional parity isn't the same as UX quality, and the diaspora community using MonieWorld wasn't comparing it only to LemFi. They'd also been shaped by Revolut, Wise, and the broader class of internationally respected fintech products that set the bar in the western markets they'd migrated to. The UX standard for this audience was higher than LemFi had set it.

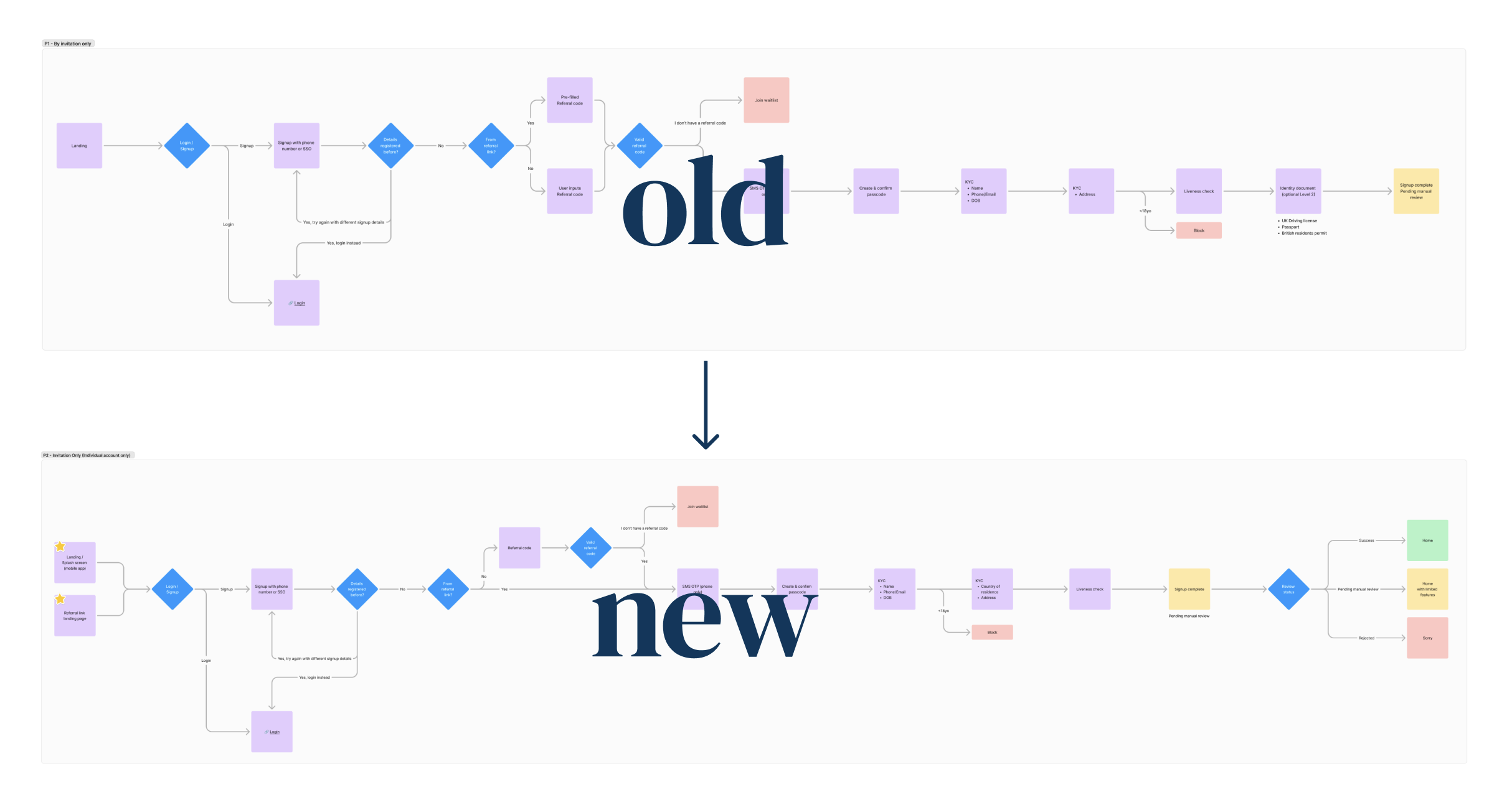

When I audited the inherited onboarding experience, the gap was clear. The original flow required users to open a GBP current account as part of signup — a requirement that added friction and wasn't legally necessary. I dug into the compliance and risk requirements and found MonieWorld was licensed to operate as a pure remittance provider: no current account opening required, and no selfie or ID upload unless automated name, date of birth, and address verification failed.

The redesigned flow strips the journey to its minimum viable steps — 29 taps from splash screen to live transfer, versus approximately 35 taps on LemFi and Wise before those products even reach selfie capture.

The redesigned flow rebuilt the onboarding experience from the ground up: cleaner hierarchy, progressive disclosure, and error states that guide rather than block. Don't ask users to do any extra upfront — build trust and habit first, then everything else follows.

84.5% signup conversion rate — compared to the industry average of 20–25% — driving 20,000 unique signups in the first 3 months since launch (Apr–Jun 2025).

29 taps from signup splash to live transfer, versus ~35 taps on LemFi and Wise before selfie and ID.

#2 · Home & Dashboard

A home screen that does one thing well: get money moving.

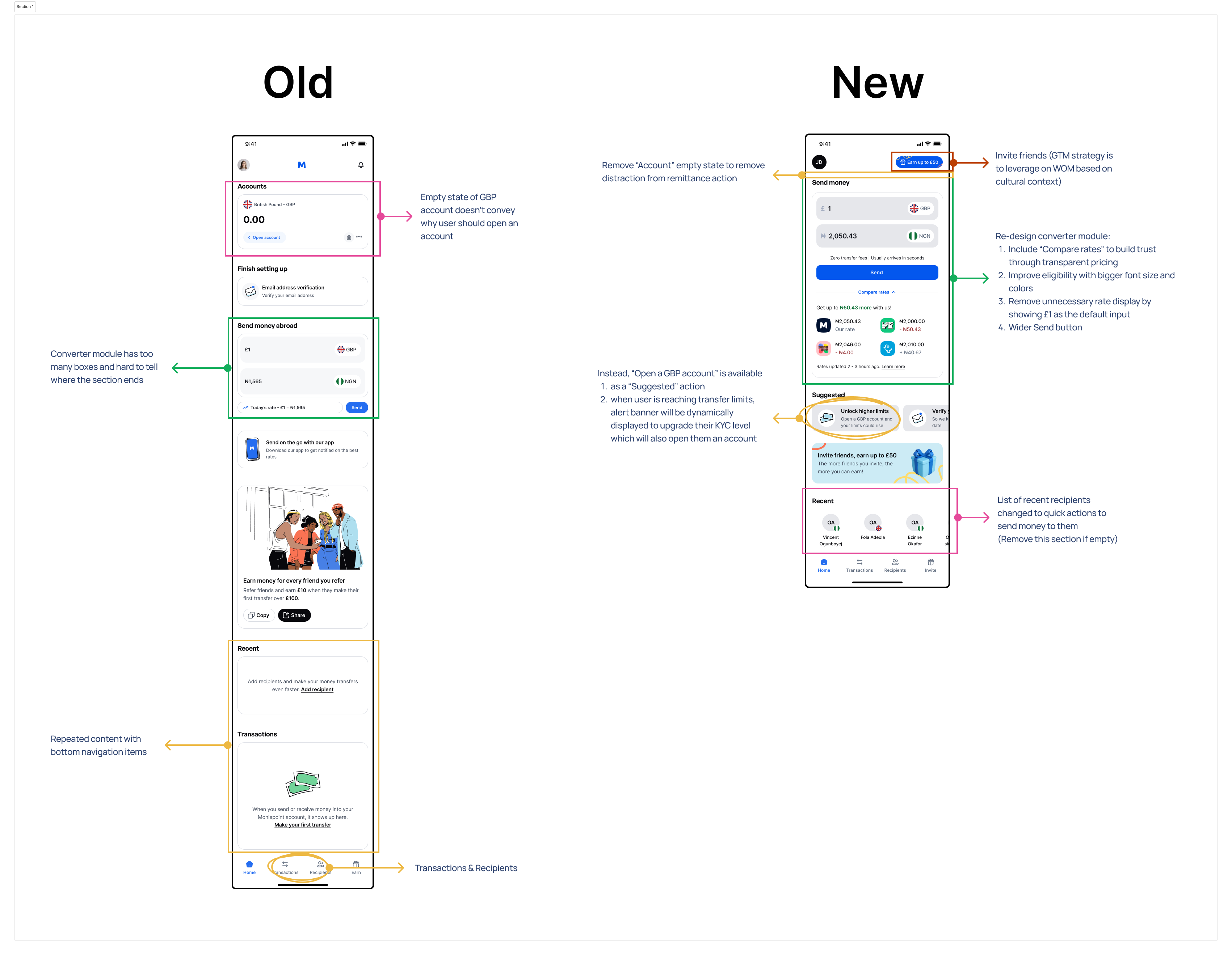

Once users arrived on the home screen after a clean signup, the dashboard needed to convert that momentum into action. The existing design had three problems that worked against this.

The GBP account empty state occupied the top of the screen with a £0.00 balance and no meaningful call to action — it made the app feel broken before the user had done anything. The send money converter module stacked too many visual boxes together, with unclear boundaries between sections and no obvious anchor for the eye. And the home feed repeated content already accessible from the bottom navigation, creating circular journeys that went nowhere.

Annotated audit of the existing home screen, highlighting the account empty state dead-end, converter clutter, and navigation redundancy.

The redesign made four focused changes:

Remove the account empty state. The GBP account module disappears from the default home view. Account opening is instead offered as a contextual action — surfaced in a "Suggested" strip when users first land, and as a dynamic upgrade prompt when they approach transfer limits. The home screen leads with the converter, because sending money is why users are here.

Rebuild the converter from first principles. A single £1 default input, the live exchange rate displayed prominently, a "Compare rates" link to build trust through transparency, and a wider Send button that's harder to mis-tap. Clarity over cleverness.

Replace the transactions list with quick-send recipients. The most common user action after signup is sending to someone specific. The recent section now shows recipient shortcuts — the people the user sends to most — and removes itself entirely on an empty state so the UI never feels hollow.

Make the GTM strategy visible. An "Invite friends, earn up to £50" banner was intentionally placed at the end of the home feed, leaning into the diaspora's word-of-mouth culture as an organic growth lever.

Home screen actively converts post-signup users into their first transfer — the activation event that defines early retention. 56.6% of users completed their first transaction within 7 days of signup across the first 3 months since launch (Apr–Jun 2025).

Contextual GBP account prompt replaced a static dead-end, surfacing the right upsell at the right moment without disrupting the primary send journey.

#3 · Information Architecture

Designing a structure that amplifies Send & Spend — and grows with the product.

MonieWorld launched as a single-purpose remittance product. The roadmap moved quickly. Cards, NGN wallets, unrestricted local transfers, scheduled payments, local and international bill payments, and FX conversion orders were all incoming. The existing information architecture — four tabs structured around the initial feature set — would not hold that weight.

My design strategy was built around a single question: what are users actually trying to do? The answer was always one of two things — send money, or spend money. Every feature, existing or incoming, maps to one of those two propositions. The new IA organises the app around Send and Spend as the primary axes, not by product category or technical implementation.

Information Architecture 2.0 — interactive prototype

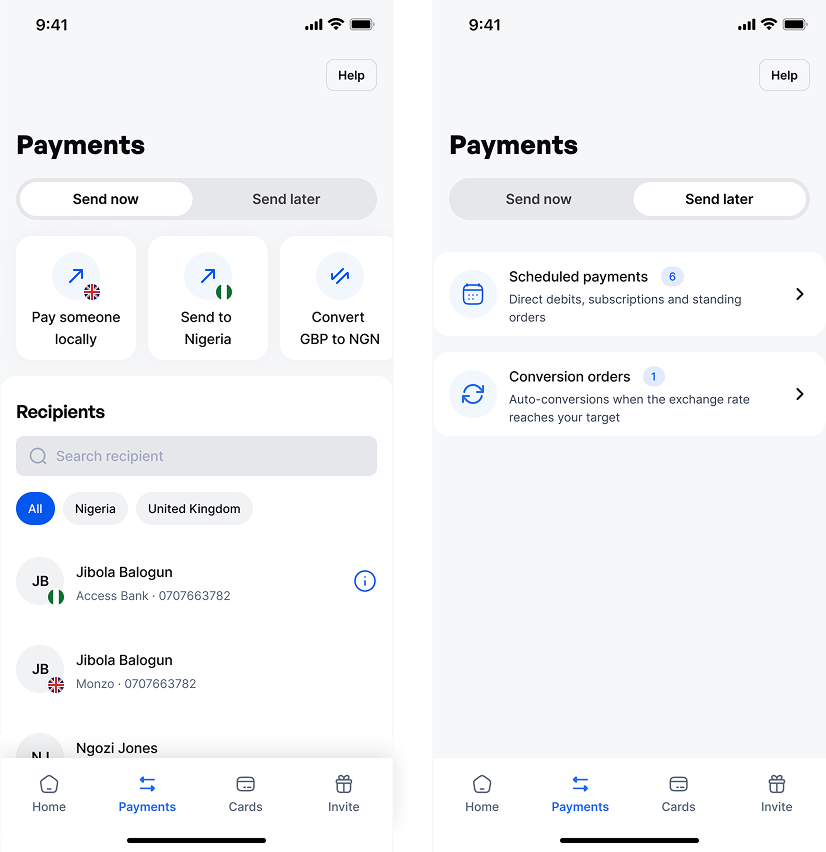

The Payments tab becomes the hub for both immediate and scheduled money movement. Send now consolidates remittance to Nigeria, local GBP payments, FX conversion into a MonieWorld NGN account, and recipient management in one place. Send later adds direct debits, standing orders, subscriptions, and conversion limit orders as the roadmap delivers them — without adding new nav items.

Home becomes a command centre: the converter front and centre, a Suggested strip that adapts to the user's activation state, and a Promo area for contextual upsells. Cards and wallets — GBP and NGN — sit within an Accounts layer, surfaced progressively as users unlock them through KYC steps, so the app never feels empty at any stage of the user lifecycle.

The redesigned Payments tab, consolidating all money movement under a unified Send now / Send later architecture.

The structure was also designed with engineering in mind. Features can be added to the Payments hub or the Suggested strip without restructuring the navigation. Empty states are handled gracefully at every layer, so the app feels considered and complete even while the roadmap is still in flight.

Outcome

A navigation framework that scales from single-product to full-suite without structural change. NGN wallet and scheduled payments — the two nearest roadmap items — slot directly into the new Payments hub without requiring additional nav items or new patterns.